6.8 Exercises

Exercise 8

library("ISLR")

library("leaps")

library("glmnet")

## Loading required package: Matrix

## Loading required package: foreach

## Loaded glmnet 2.0-2

set.seed(0)

n <- 100

X <- rnorm(n)

epsilon <- 0.1 * rnorm(n)

beta_0 <- 1

beta_1 <- -0.1

beta_2 <- +0.05

beta_3 <- 0.75

Y <- beta_0 + beta_1 * X + beta_2 * X^2 + beta_3 * X^3 + epsilon

DF <- data.frame(Y = Y, X = X, X2 = X^2, X3 = X^3, X4 = X^4, X5 = X^5, X6 = X^6, X7 = X^7, X8 = X^8, X9 = X^9, X10 = X^10)

train <- sample(c(TRUE, FALSE), n, rep = TRUE)

test <- (!train)

regfit.full <- regsubsets(Y ~ ., data = DF[train, ], nvmax = 10)

print(summary(regfit.full))

## Subset selection object

## Call: regsubsets.formula(Y ~ ., data = DF[train, ], nvmax = 10)

## 10 Variables (and intercept)

## Forced in Forced out

## X FALSE FALSE

## X2 FALSE FALSE

## X3 FALSE FALSE

## X4 FALSE FALSE

## X5 FALSE FALSE

## X6 FALSE FALSE

## X7 FALSE FALSE

## X8 FALSE FALSE

## X9 FALSE FALSE

## X10 FALSE FALSE

## 1 subsets of each size up to 10

## Selection Algorithm: exhaustive

## X X2 X3 X4 X5 X6 X7 X8 X9 X10

## 1 ( 1 ) " " " " "*" " " " " " " " " " " " " " "

## 2 ( 1 ) "*" " " "*" " " " " " " " " " " " " " "

## 3 ( 1 ) "*" "*" "*" " " " " " " " " " " " " " "

## 4 ( 1 ) " " "*" "*" " " "*" " " "*" " " " " " "

## 5 ( 1 ) " " "*" "*" "*" "*" " " " " " " "*" " "

## 6 ( 1 ) " " "*" "*" " " "*" "*" " " "*" "*" " "

## 7 ( 1 ) "*" "*" "*" " " "*" "*" " " "*" "*" " "

## 8 ( 1 ) " " "*" "*" " " "*" "*" "*" "*" "*" "*"

## 9 ( 1 ) "*" "*" "*" " " "*" "*" "*" "*" "*" "*"

## 10 ( 1 ) "*" "*" "*" "*" "*" "*" "*" "*" "*" "*"

reg.summary <- summary(regfit.full)

test.mat <- model.matrix(Y ~ ., data = DF[test, ])

val.errors <- rep(NA, 10)

for (ii in 1:10) {

coefi <- coef(regfit.full, id = ii)

pred <- test.mat[, names(coefi)] %*% coefi

val.errors[ii] <- mean((DF$Y[test] - pred)^2)

}

print("best subset validation errors")

## [1] "best subset validation errors"

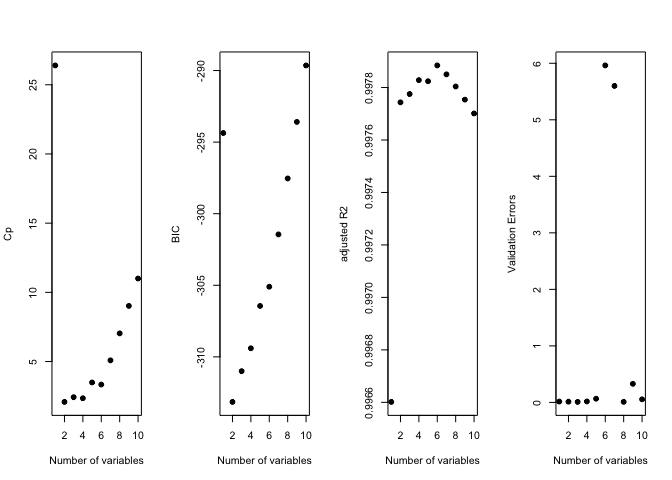

print(val.errors)

## [1] 0.015567409 0.013245221 0.009026844 0.017169840 0.065102301

## [6] 5.962097578 5.599171828 0.010197576 0.328677632 0.055217617

k <- which.min(val.errors)

print(k)

## [1] 3

print(coef(regfit.full, id = k))

## (Intercept) X X2 X3

## 1.01506706 -0.11855671 0.02753875 0.76721123

old.par <- par(mfrow = c(1, 4))

plot(reg.summary$cp, xlab = "Number of variables", ylab = "Cp", pch = 19)

plot(reg.summary$bic, xlab = "Number of variables", ylab = "BIC", pch = 19)

plot(reg.summary$adjr2, xlab = "Number of variables", ylab = "adjusted R2", pch = 19)

plot(val.errors, xlab = "Number of variables", ylab = "Validation Errors", pch = 19)

par(mfrow = c(1, 1))

regfit.forward <- regsubsets(Y ~ ., data = DF[train, ], nvmax = 10, method = "forward")

print(summary(regfit.forward))

## Subset selection object

## Call: regsubsets.formula(Y ~ ., data = DF[train, ], nvmax = 10, method = "forward")

## 10 Variables (and intercept)

## Forced in Forced out

## X FALSE FALSE

## X2 FALSE FALSE

## X3 FALSE FALSE

## X4 FALSE FALSE

## X5 FALSE FALSE

## X6 FALSE FALSE

## X7 FALSE FALSE

## X8 FALSE FALSE

## X9 FALSE FALSE

## X10 FALSE FALSE

## 1 subsets of each size up to 10

## Selection Algorithm: forward

## X X2 X3 X4 X5 X6 X7 X8 X9 X10

## 1 ( 1 ) " " " " "*" " " " " " " " " " " " " " "

## 2 ( 1 ) "*" " " "*" " " " " " " " " " " " " " "

## 3 ( 1 ) "*" "*" "*" " " " " " " " " " " " " " "

## 4 ( 1 ) "*" "*" "*" "*" " " " " " " " " " " " "

## 5 ( 1 ) "*" "*" "*" "*" "*" " " " " " " " " " "

## 6 ( 1 ) "*" "*" "*" "*" "*" " " " " " " "*" " "

## 7 ( 1 ) "*" "*" "*" "*" "*" " " " " "*" "*" " "

## 8 ( 1 ) "*" "*" "*" "*" "*" "*" " " "*" "*" " "

## 9 ( 1 ) "*" "*" "*" "*" "*" "*" "*" "*" "*" " "

## 10 ( 1 ) "*" "*" "*" "*" "*" "*" "*" "*" "*" "*"

reg.summary <- summary(regfit.forward)

test.mat <- model.matrix(Y ~ ., data = DF[test, ])

val.errors <- rep(NA, 10)

for (ii in 1:10) {

coefi <- coef(regfit.forward, id = ii)

pred <- test.mat[, names(coefi)] %*% coefi

val.errors[ii] <- mean((DF$Y[test] - pred)^2)

}

print("forward selection validation errors")

## [1] "forward selection validation errors"

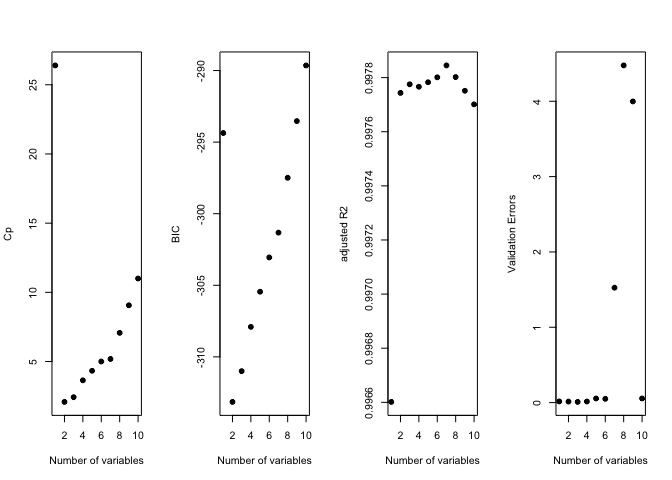

print(val.errors)

## [1] 0.015567409 0.013245221 0.009026844 0.014540813 0.055005227

## [6] 0.049894349 1.525498490 4.476027607 3.997884857 0.055217617

k <- which.min(val.errors)

print(k)

## [1] 3

print(coef(regfit.forward, id = k))

## (Intercept) X X2 X3

## 1.01506706 -0.11855671 0.02753875 0.76721123

old.par <- par(mfrow = c(1, 4))

plot(reg.summary$cp, xlab = "Number of variables", ylab = "Cp", pch = 19)

plot(reg.summary$bic, xlab = "Number of variables", ylab = "BIC", pch = 19)

plot(reg.summary$adjr2, xlab = "Number of variables", ylab = "adjusted R2", pch = 19)

plot(val.errors, xlab = "Number of variables", ylab = "Validation Errors", pch = 19)

par(mfrow = c(1, 1))

regfit.backward <- regsubsets(Y ~ ., data = DF[train, ], nvmax = 10, method = "backward")

print(summary(regfit.backward))

## Subset selection object

## Call: regsubsets.formula(Y ~ ., data = DF[train, ], nvmax = 10, method = "backward")

## 10 Variables (and intercept)

## Forced in Forced out

## X FALSE FALSE

## X2 FALSE FALSE

## X3 FALSE FALSE

## X4 FALSE FALSE

## X5 FALSE FALSE

## X6 FALSE FALSE

## X7 FALSE FALSE

## X8 FALSE FALSE

## X9 FALSE FALSE

## X10 FALSE FALSE

## 1 subsets of each size up to 10

## Selection Algorithm: backward

## X X2 X3 X4 X5 X6 X7 X8 X9 X10

## 1 ( 1 ) " " " " "*" " " " " " " " " " " " " " "

## 2 ( 1 ) " " " " "*" " " "*" " " " " " " " " " "

## 3 ( 1 ) "*" "*" "*" " " " " " " " " " " " " " "

## 4 ( 1 ) " " "*" "*" " " "*" " " "*" " " " " " "

## 5 ( 1 ) " " "*" "*" " " "*" "*" "*" " " " " " "

## 6 ( 1 ) " " "*" "*" " " "*" "*" "*" "*" " " " "

## 7 ( 1 ) " " "*" "*" " " "*" "*" "*" "*" " " "*"

## 8 ( 1 ) " " "*" "*" " " "*" "*" "*" "*" "*" "*"

## 9 ( 1 ) "*" "*" "*" " " "*" "*" "*" "*" "*" "*"

## 10 ( 1 ) "*" "*" "*" "*" "*" "*" "*" "*" "*" "*"

reg.summary <- summary(regfit.backward)

test.mat <- model.matrix(Y ~ ., data = DF[test, ])

val.errors <- rep(NA, 10)

for (ii in 1:10) {

coefi <- coef(regfit.backward, id = ii)

pred <- test.mat[, names(coefi)] %*% coefi

val.errors[ii] <- mean((DF$Y[test] - pred)^2)

}

print("backwards selection validation errors")

## [1] "backwards selection validation errors"

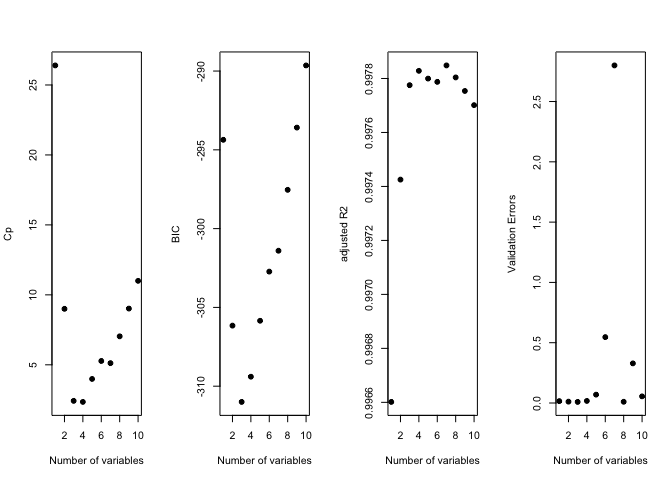

print(val.errors)

## [1] 0.015567409 0.011250512 0.009026844 0.017169840 0.069259376

## [6] 0.546418670 2.799471622 0.010197576 0.328677632 0.055217617

k <- which.min(val.errors)

print(k)

## [1] 3

print(coef(regfit.backward, id = k))

## (Intercept) X X2 X3

## 1.01506706 -0.11855671 0.02753875 0.76721123

old.par <- par(mfrow = c(1, 4))

plot(reg.summary$cp, xlab = "Number of variables", ylab = "Cp", pch = 19)

plot(reg.summary$bic, xlab = "Number of variables", ylab = "BIC", pch = 19)

plot(reg.summary$adjr2, xlab = "Number of variables", ylab = "adjusted R2", pch = 19)

plot(val.errors, xlab = "Number of variables", ylab = "Validation Errors", pch = 19)

par(mfrow = c(1, 1))

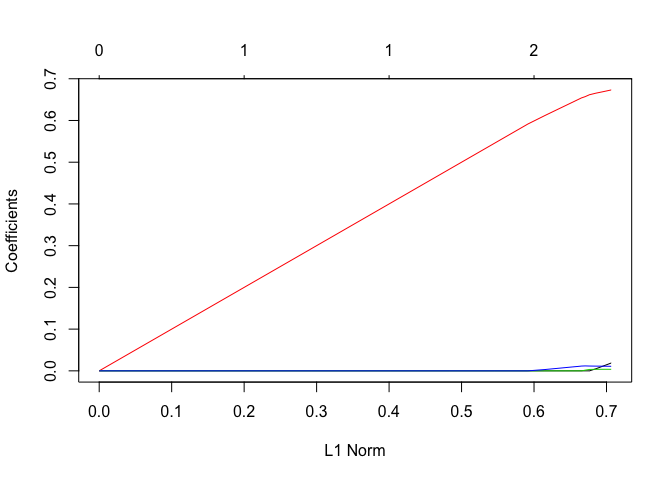

grid <- 10^seq(10, -2, length = 100)

Y <- DF$Y

MM <- model.matrix(Y ~ ., data = DF)

lasso.mod <- glmnet(MM, Y, alpha = 1, lambda = grid)

plot(lasso.mod)

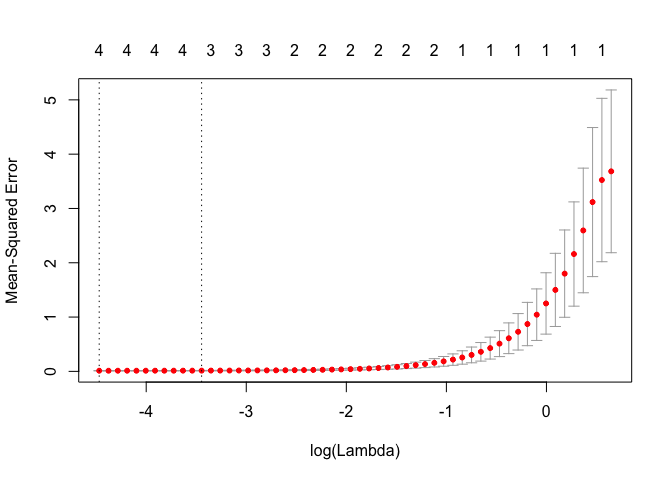

cv.out <- cv.glmnet(MM, Y, alpha = 1)

bestlam <- cv.out$lambda.1se

print("lasso CV best value of lambda (one standard error)")

## [1] "lasso CV best value of lambda (one standard error)"

print(bestlam)

## [1] 0.03186245

plot(cv.out)

lasso.coef <- predict(lasso.mod, type = "coefficients", s = bestlam)

print(lasso.coef)

## 12 x 1 sparse Matrix of class "dgCMatrix"

## 1

## (Intercept) 1.026020037

## (Intercept) .

## X .

## X2 0.004179690

## X3 0.664868098

## X4 0.003606719

## X5 0.011344145

## X6 .

## X7 .

## X8 .

## X9 .

## X10 .

X <- rnorm(n)

epsilon <- 0.1 * rnorm(n)

beta_0 <- 1

beta_7 <- 2.5

Y <- beta_0 + beta_7 * X^7 + epsilon

DF <- data.frame(Y = Y, X = X, X2 = X^2, X3 = X^3, X4 = X^4, X5 = X^5, X6 = X^6, X7 = X^7, X8 = X^8, X9 = X^9, X10 = X^10)

train <- sample(c(TRUE, FALSE), n, rep = TRUE)

test <- (!train)

regfit.full <- regsubsets(Y ~ ., data = DF[train, ], nvmax = 10)

print(summary(regfit.full))

## Subset selection object

## Call: regsubsets.formula(Y ~ ., data = DF[train, ], nvmax = 10)

## 10 Variables (and intercept)

## Forced in Forced out

## X FALSE FALSE

## X2 FALSE FALSE

## X3 FALSE FALSE

## X4 FALSE FALSE

## X5 FALSE FALSE

## X6 FALSE FALSE

## X7 FALSE FALSE

## X8 FALSE FALSE

## X9 FALSE FALSE

## X10 FALSE FALSE

## 1 subsets of each size up to 10

## Selection Algorithm: exhaustive

## X X2 X3 X4 X5 X6 X7 X8 X9 X10

## 1 ( 1 ) " " " " " " " " " " " " "*" " " " " " "

## 2 ( 1 ) "*" " " " " " " " " " " "*" " " " " " "

## 3 ( 1 ) "*" " " " " " " "*" " " "*" " " " " " "

## 4 ( 1 ) " " " " "*" " " "*" " " "*" " " "*" " "

## 5 ( 1 ) " " " " "*" "*" "*" " " "*" " " "*" " "

## 6 ( 1 ) " " " " " " " " "*" "*" "*" "*" "*" "*"

## 7 ( 1 ) " " "*" " " "*" "*" "*" "*" " " "*" "*"

## 8 ( 1 ) "*" "*" " " "*" "*" "*" "*" " " "*" "*"

## 9 ( 1 ) "*" "*" "*" "*" "*" "*" "*" " " "*" "*"

## 10 ( 1 ) "*" "*" "*" "*" "*" "*" "*" "*" "*" "*"

test.mat <- model.matrix(Y ~ ., data = DF[test, ])

val.errors <- rep(NA, 10)

for (ii in 1:10) {

coefi <- coef(regfit.full, id = ii)

pred <- test.mat[, names(coefi)] %*% coefi

val.errors[ii] <- mean((DF$Y[test] - pred)^2)

}

print("best subsets validation errors")

## [1] "best subsets validation errors"

print(val.errors)

## [1] 0.01151953 0.01334971 0.01514501 0.06420174 0.09905791 1.86716273

## [7] 0.62617621 0.58059869 0.53819549 1.05507636

k <- which.min(val.errors)

print(k)

## [1] 1

print("best subsets optimal coefficients")

## [1] "best subsets optimal coefficients"

print(coef(regfit.full, id = k))

## (Intercept) X7

## 0.9840339 2.5000261

print(val.errors[k])

## [1] 0.01151953

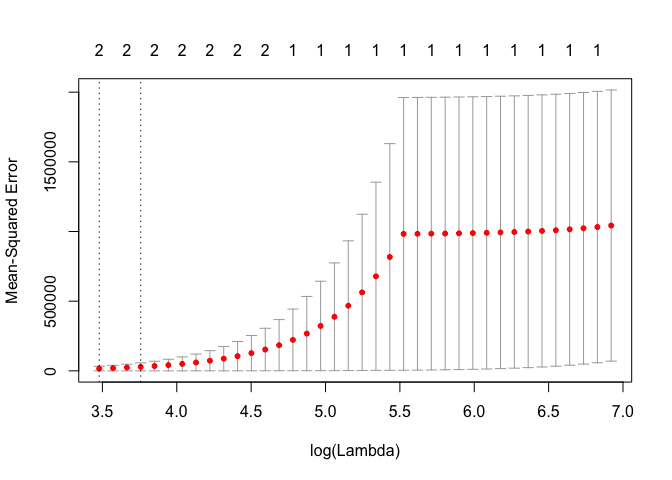

MM <- model.matrix(Y ~ ., data = DF)

cv.out <- cv.glmnet(MM, Y, alpha = 1)

plot(cv.out)

bestlam <- cv.out$lambda.1se

print("best lambda (1 se)")

## [1] "best lambda (1 se)"

print(bestlam)

## [1] 42.84324

lasso.mod <- glmnet(MM, Y, alpha = 1)

lasso.coef <- predict(lasso.mod, type = "coefficients", s = bestlam)

print("lasso optimal coefficients")

## [1] "lasso optimal coefficients"

print(lasso.coef)

## 12 x 1 sparse Matrix of class "dgCMatrix"

## 1

## (Intercept) 5.3888292

## (Intercept) .

## X .

## X2 .

## X3 .

## X4 .

## X5 .

## X6 0.2125842

## X7 2.3286883

## X8 .

## X9 .

## X10 .

print("I do not think the predict method is working correctly...")

## [1] "I do not think the predict method is working correctly..."

lasso.predict <- predict(lasso.mod, s = bestlam, newx = MM)

print("lasso RSS error")

## [1] "lasso RSS error"

print(mean((Y - lasso.predict)^2))

## [1] 1839.887

Exercise 9

library(pls)

##

## Attaching package: 'pls'

##

## The following object is masked from 'package:stats':

##

## loadings

set.seed(0)

n <- dim(College)[1]

p <- dim(College)[2]

train <- sample(c(TRUE, FALSE), n, rep = TRUE)

test <- (!train)

College_train <- College[train, ]

College_test <- College[test, ]

m <- lm(Apps ~ ., data = College_train)

Y_hat <- predict(m, newdata = College_test)

MSE <- mean((College_test$Apps - Y_hat)^2)

print(sprintf("Linear model test MSE= %10.3f", MSE))

## [1] "Linear model test MSE= 1615966.966"

Y <- College_train$Apps

MM <- model.matrix(Apps ~ ., data = College_train)

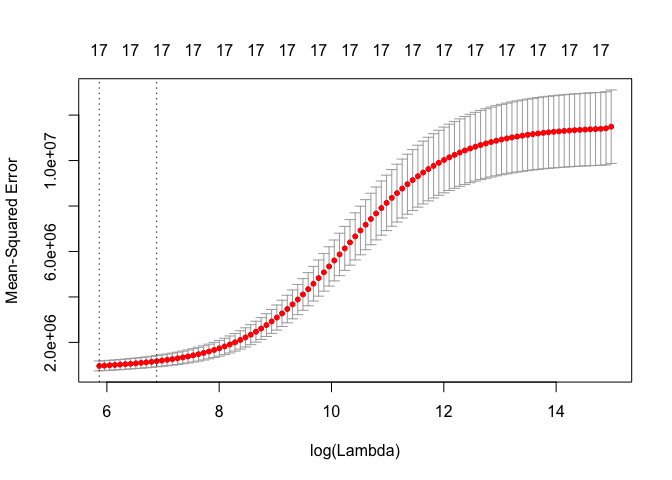

cv.out <- cv.glmnet(MM, Y, alpha = 0)

plot(cv.out)

bestlam <- cv.out$lambda.1se

ridge.mod <- glmnet(MM, Y, alpha = 0)

Y_hat <- predict(ridge.mod, s = bestlam, newx = model.matrix(Apps ~ ., data = College_test))

MSE <- mean((College_test$Apps - Y_hat)^2)

print(sprintf("Ridge regression test MSE= %10.3f", MSE))

## [1] "Ridge regression test MSE= 3318015.663"

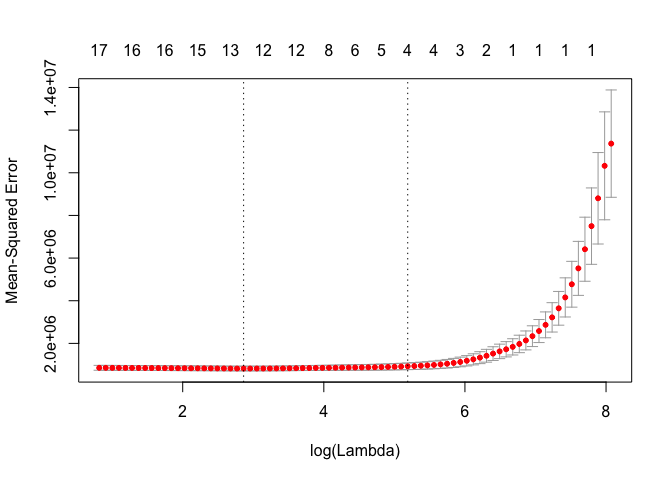

cv.out <- cv.glmnet(MM, Y, alpha = 1)

plot(cv.out)

bestlam <- cv.out$lambda.1se

lasso.mod <- glmnet(MM, Y, alpha = 1)

Y_hat <- predict(lasso.mod, s = bestlam, newx = model.matrix(Apps ~ ., data = College_test))

MSE <- mean((College_test$Apps - Y_hat)^2)

print(sprintf("Lasso regression test MSE= %10.3f", MSE))

## [1] "Lasso regression test MSE= 2018489.732"

print("lasso coefficients")

## [1] "lasso coefficients"

print(predict(lasso.mod, type = "coefficients", s = bestlam))

## 19 x 1 sparse Matrix of class "dgCMatrix"

## 1

## (Intercept) -515.67319420

## (Intercept) .

## PrivateYes .

## Accept 1.26431392

## Enroll .

## Top10perc 14.89903622

## Top25perc .

## F.Undergrad 0.01925533

## P.Undergrad .

## Outstate .

## Room.Board .

## Books .

## Personal .

## PhD .

## Terminal .

## S.F.Ratio .

## perc.alumni .

## Expend 0.04586867

## Grad.Rate .

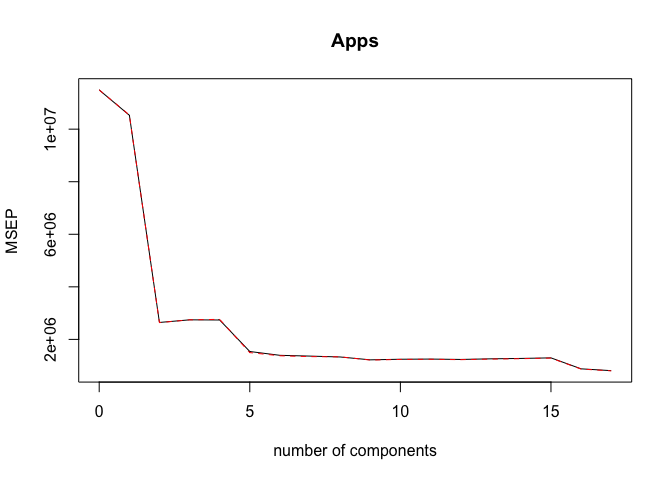

pcr.mod <- pcr(Apps ~ ., data = College_train, scale = TRUE, validation = "CV")

validationplot(pcr.mod, val.type = "MSEP")

ncomp <- 17

Y_hat <- predict(pcr.mod, College_test, ncomp = ncomp)

MSE <- mean((College_test$Apps - Y_hat)^2)

print(sprintf("PCR (with ncomp= %5d) test MSE= %10.3f", ncomp, MSE))

## [1] "PCR (with ncomp= 17) test MSE= 1615966.966"

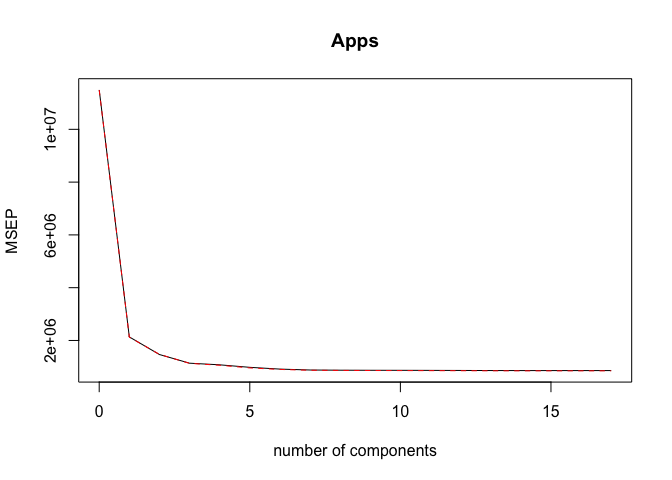

pls.mod <- plsr(Apps ~ ., data = College_train, scale = TRUE, validation = "CV")

validationplot(pls.mod, val.type = "MSEP")

ncomp <- 10

Y_hat <- predict(pls.mod, College_test, ncomp = ncomp)

MSE <- mean((College_test$Apps - Y_hat)^2)

print(sprintf("PLS (with ncomp= %5d) test MSE= %10.3f", ncomp, MSE))

## [1] "PLS (with ncomp= 10) test MSE= 1601425.747"

Exercise 10

set.seed(0)

n <- 1000

p <- 20

beta_truth <- rnorm(p + 1)

zero_locations <- c(2, 3, 4, 7, 8, 11, 12, 15, 17, 20)

beta_truth[zero_locations] <- 0

print("True values for beta (beta_0-beta_20):")

## [1] "True values for beta (beta_0-beta_20):"

print(beta_truth)

## [1] 1.262954285 0.000000000 0.000000000 0.000000000 0.414641434

## [6] -1.539950042 0.000000000 0.000000000 -0.005767173 2.404653389

## [11] 0.000000000 0.000000000 -1.147657009 -0.289461574 0.000000000

## [16] -0.411510833 0.000000000 -0.891921127 0.435683299 0.000000000

## [21] -0.224267885

X <- c(rep(1, n), rnorm(n * p))

X <- matrix(X, nrow = n, ncol = (p + 1), byrow = FALSE)

Y <- X %*% beta_truth + rnorm(n)

DF <- data.frame(Y, X[, -1])

train_inds <- sample(1:n, 100)

test_inds <- (1:n)[-train_inds]

regfit.full <- regsubsets(Y ~ ., data = DF[train_inds, ], nvmax = 20)

reg.summary <- summary(regfit.full)

training.mat <- model.matrix(Y ~ ., data = DF[train_inds, ])

training.errors <- rep(NA, 20)

for (ii in 1:20) {

coefi <- coef(regfit.full, id = ii)

pred <- training.mat[, names(coefi)] %*% coefi

training.errors[ii] <- mean((DF$Y[train_inds] - pred)^2)

}

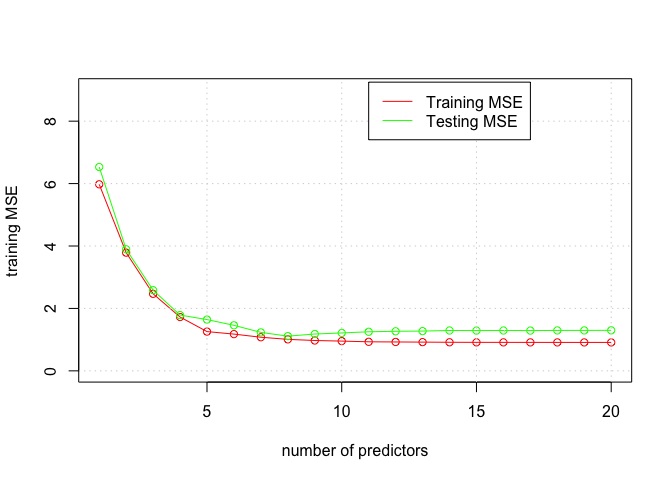

print("best subset training MSE")

## [1] "best subset training MSE"

print(training.errors)

## [1] 5.9770059 3.7871159 2.4678405 1.7251665 1.2576488 1.1772519 1.0768021

## [8] 1.0087222 0.9721521 0.9530143 0.9304660 0.9254522 0.9206935 0.9152359

## [15] 0.9133050 0.9125718 0.9117938 0.9112271 0.9108313 0.9106024

plot(1:20, training.errors, xlab = "number of predictors", ylab = "training MSE", type = "o", col = "red", ylim = c(0, 9))

test.mat <- model.matrix(Y ~ ., data = DF[test_inds, ])

val.errors <- rep(NA, 20)

for (ii in 1:20) {

coefi <- coef(regfit.full, id = ii)

pred <- test.mat[, names(coefi)] %*% coefi

val.errors[ii] <- mean((DF$Y[test_inds] - pred)^2)

}

print("best subset validation MSE")

## [1] "best subset validation MSE"

print(val.errors)

## [1] 6.531306 3.895918 2.584956 1.787702 1.642511 1.458888 1.232284

## [8] 1.111670 1.180321 1.214303 1.251878 1.267629 1.274193 1.293091

## [15] 1.290385 1.292731 1.290206 1.294843 1.295492 1.297954

k <- which.min(val.errors)

print(k)

## [1] 8

print(coef(regfit.full, id = k))

## (Intercept) X4 X5 X9 X12 X13

## 1.3210455 0.4132288 -1.5880109 2.4639393 -1.1455077 -0.2815162

## X15 X17 X18

## -0.3589236 -1.0286318 0.6142240

points(1:20, val.errors, xlab = "number of predictors", ylab = "testing MSE", type = "o", col = "green")

grid()

legend(11, 9.25, c("Training MSE", "Testing MSE"), col = c("red", "green"), lty = c(1, 1))

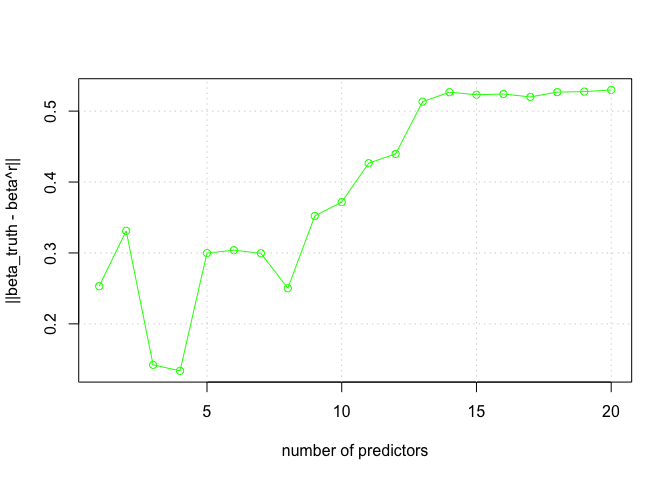

nms <- colnames(DF)

nms[1] <- "(Intercept)"

names(beta_truth) <- nms

norm.beta.diff <- rep(NA, 20)

for (ii in 1:20) {

coefi <- coef(regfit.full, id = ii)

norm.beta.diff[ii] <- sqrt(sum((beta_truth[names(coefi)] - coefi)^2))

}

plot(1:20, norm.beta.diff, xlab = "number of predictors", ylab = "||beta_truth - beta^r||", type = "o", col = "green")

grid()

Exercise 11

library(MASS)

set.seed(0)

n <- dim(Boston)[1]

p <- dim(Boston)[2]

train <- sample(c(TRUE, FALSE), n, rep = TRUE)

test <- (!train)

Boston_train <- Boston[train, ]

Boston_test <- Boston[test, ]

m <- lm(crim ~ ., data = Boston_train)

Y_hat <- predict(m, newdata = Boston_test)

MSE <- mean((Boston_test$crim - Y_hat)^2)

print(sprintf("Linear model test MSE= %10.3f", MSE))

## [1] "Linear model test MSE= 34.996"

Y <- Boston_train$crim

MM <- model.matrix(crim ~ ., data = Boston_train)

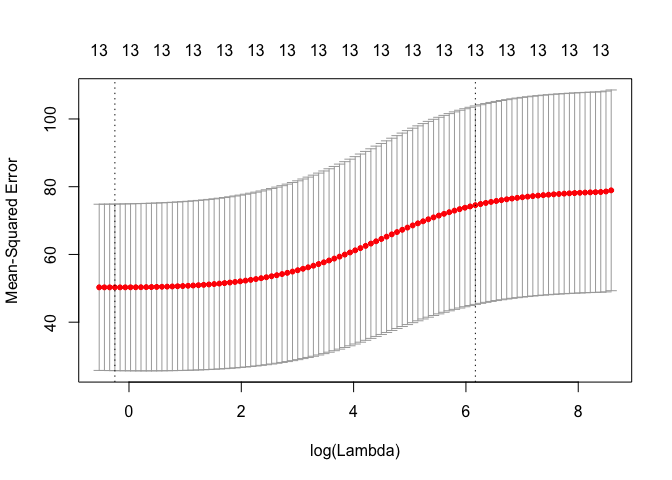

cv.out <- cv.glmnet(MM, Y, alpha = 0)

plot(cv.out)

bestlam <- cv.out$lambda.1se

ridge.mod <- glmnet(MM, Y, alpha = 0)

Y_hat <- predict(ridge.mod, s = bestlam, newx = model.matrix(crim ~ ., data = Boston_test))

MSE <- mean((Boston_test$crim - Y_hat)^2)

print(sprintf("Ridge regression test MSE= %10.3f", MSE))

## [1] "Ridge regression test MSE= 63.826"

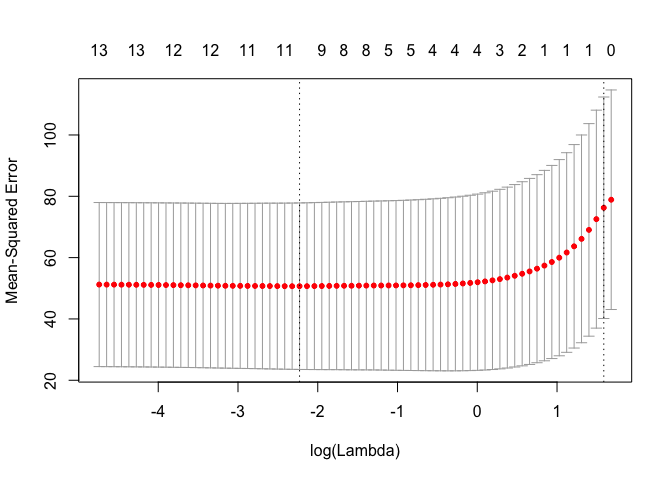

cv.out <- cv.glmnet(MM, Y, alpha = 1)

plot(cv.out)

bestlam <- cv.out$lambda.1se

lasso.mod <- glmnet(MM, Y, alpha = 1)

Y_hat <- predict(lasso.mod, s = bestlam, newx = model.matrix(crim ~ ., data = Boston_test))

MSE <- mean((Boston_test$crim - Y_hat)^2)

print(sprintf("Lasso regression test MSE= %10.3f", MSE))

## [1] "Lasso regression test MSE= 63.572"

print("lasso coefficients")

## [1] "lasso coefficients"

print(predict(lasso.mod, type = "coefficients", s = bestlam))

## 15 x 1 sparse Matrix of class "dgCMatrix"

## 1

## (Intercept) 3.07011734

## (Intercept) .

## zn .

## indus .

## chas .

## nox .

## rm .

## age .

## dis .

## rad 0.05507813

## tax .

## ptratio .

## black .

## lstat .

## medv .

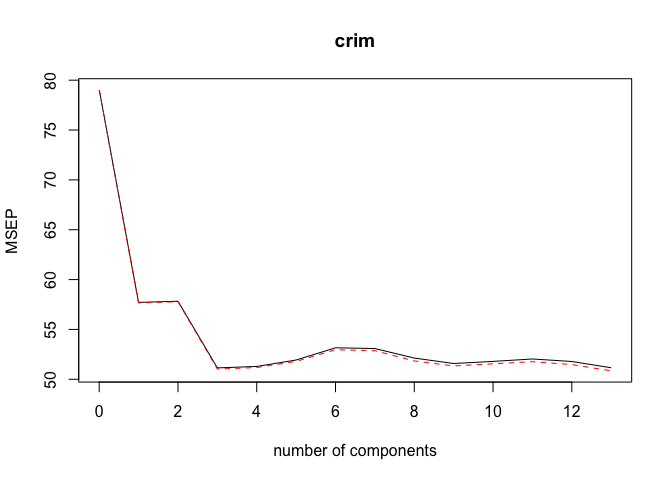

pcr.mod <- pcr(crim ~ ., data = Boston_train, scale = TRUE, validation = "CV")

validationplot(pcr.mod, val.type = "MSEP")

ncomp <- 3

Y_hat <- predict(pcr.mod, Boston_test, ncomp = ncomp)

MSE <- mean((Boston_test$crim - Y_hat)^2)

print(sprintf("PCR (with ncomp= %5d) test MSE= %10.3f", ncomp, MSE))

## [1] "PCR (with ncomp= 3) test MSE= 40.049"

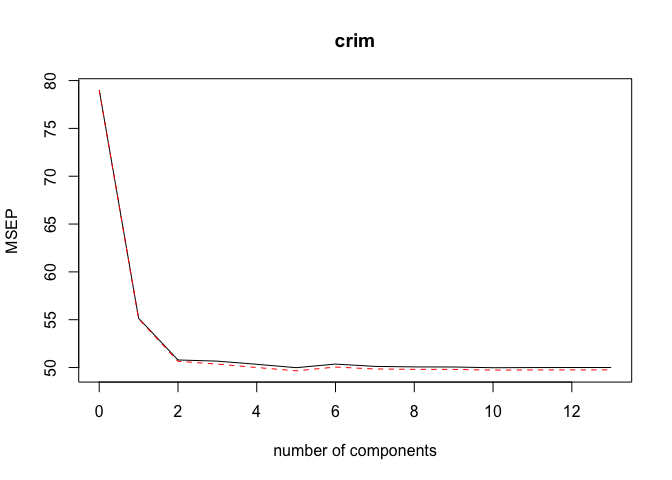

pls.mod <- plsr(crim ~ ., data = Boston_train, scale = TRUE, validation = "CV")

validationplot(pls.mod, val.type = "MSEP")

ncomp <- 5

Y_hat <- predict(pls.mod, Boston_test, ncomp = ncomp)

MSE <- mean((Boston_test$crim - Y_hat)^2)

print(sprintf("PLS (with ncomp= %5d) test MSE= %10.3f", ncomp, MSE))

## [1] "PLS (with ncomp= 5) test MSE= 35.258"